When a Painting Returns 3,500%

Why spectacular art-market returns happen — and why they're the least important part of the story.

Every once in a while, a number escapes the art world and lands squarely in the financial press.

This week it was 3,500%.

According to a recent Bloomberg report on the sale, British billionaire collector Joe Lewis achieved returns exceeding 3,500% after selling several works from his long-held collection at a Sotheby's evening sale in London. The paintings — by Francis Bacon, Lucian Freud, and Leon Kossoff — had been acquired decades earlier and only recently returned to the market.

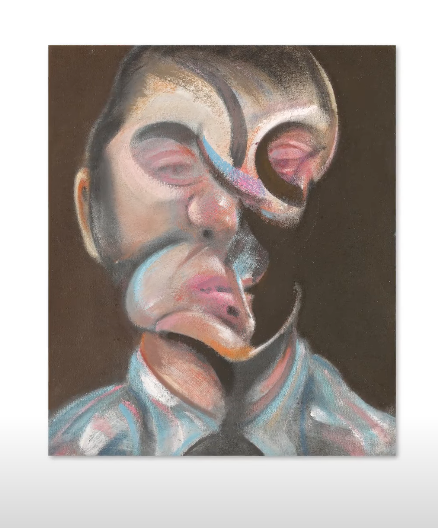

One work illustrates the scale of the appreciation. A 1972 self-portrait by Francis Bacon that Lewis bought in the 1990s for roughly £364,500 sold for £13.5 million, beating its estimate and multiplying the original purchase price many times over.

The headline writes itself:

Art delivers a 3,500% return.

But that number tells a misleading story.

Because returns like this are not a strategy.

They're an outcome.

The Conditions That Produce Returns Like This

In the financial world, extraordinary gains usually suggest timing or skill.

In the art market, they usually suggest time.

The works Lewis sold had been in his collection for nearly thirty years before appearing again at auction.

That span matters more than almost anything else.

Over the course of three decades:

• artists pass through major museum retrospectives • scholars publish definitive monographs • collectors absorb the best works into long-term holdings • supply in the open market quietly disappears

By the time a painting resurfaces, the object has changed categories.

It is no longer simply a work by a good artist.

It has become a historical example of a canonical one.

The School of London Moment

The works Lewis sold came from artists associated with the School of London — a group of postwar painters including Bacon, Freud, and Kossoff who insisted on figurative painting at a time when abstraction dominated much of the art world.

Their paintings are psychologically intense and materially heavy with paint. Bodies twist. Faces distort. Rooms feel compressed with emotion.

At the time many collectors began acquiring these works in the late twentieth century, their long-term place in art history was still forming.

Over the decades that followed, the picture sharpened.

Lucian Freud work, studio, portrait

Museums organized major exhibitions. Institutional collections deepened their holdings. Art historians clarified their significance within postwar painting.

Eventually, the market aligned with that institutional recognition.

When it does, the result can look dramatic on paper.

A Headline vs. a Lifetime

The Bloomberg article framed the sale with a telling line:

"The Tavistock Group founder notched gains of more than 3,500% through offloading long-held parts of his art collection."

The key phrase there is long-held.

That's the part the headlines tend to glide past.

Thirty years is longer than most investment strategies survive. Longer than many gallery programs last. Longer than most collectors hold onto a single work.

And yet that duration is exactly what allowed the paintings to accumulate historical weight.

The market didn't create the value.

Time did.

Why the Percentage Isn't the Point

Stories like this often circulate as proof that art can outperform other assets.

But the reality is more complicated.

Returns like this depend on a convergence of factors that are difficult — if not impossible — to engineer:

• the right artist • the right period of the artist's career • the right moment in art history • decades of patience

Most collectors who build meaningful collections aren't chasing that equation.

They're responding to something else entirely.

Curiosity. Conviction. A desire to live with objects that expand the way they see the world.

Ironically, those motivations tend to produce the strongest collections.

Because collectors who buy that way do two things the market eventually rewards.

They buy what they believe in.

And they keep it long enough for the rest of the world to understand why.

The Return That Matters

Financial headlines can measure appreciation.

They cannot measure what it means to live with a painting for thirty years — to watch it appear in exhibitions, see it discussed in scholarship, and recognize it when art history begins to consolidate around it.

The financial return arrives at the end of that process.

But it is almost never the reason the process begins.

Footnote: Benjamin Stupples, "Billionaire Joe Lewis Scores 3,500% Return on 'Masterpieces' Art," Bloomberg, March 7, 2026.