The Art Market's Attention Problem

Why market visibility is rising while participation (and real results) remain small

The art world has never been more visible.

Sitting here with my cup of coffee, I'm scrolling through my 40 new artsy alerts, a feed of museum shows, emerging painters, high-brow criticism, gallery footage, on and on and on.

Headlines read: new record price! Sold out! Never-before-seen!

Art fairs draw record crowds. Instagram circulates artworks across continents in seconds. Auction databases catalogue millions of results, building an ever-expanding record of the market's activity.

Yet the number of people actually buying art remains surprisingly small.

In his essay The Art Market's Great Illusion: Attention Is Not Liquidity, collector and entrepreneur Sylvain Lévy argues that the art world has confused two very different things.

"We have mistaken the scale of our audiences for the depth of our participation."

The industry has perfected the spectacle of cultural attention. But attention, as Lévy points out, is not the same as demand.

At Art Basel Miami Beach, he cites, fewer than 1% of visitors purchase a work.

Art Basel, Miami Beach, 2024. Photo: Art Basel.

For comparison, luxury retail conversion rates typically range between 20–30%.

The art world has built a remarkably effective attention machine—but a much smaller ecosystem of buyers.

The Illusion of Scale

The numbers behind the global art market reveal a striking paradox.

As we digest the 2025 data in detail, the trends appear to be about the same.

Reading the Art Market Reports

In 2024, more than 1.2 million works were offered at auction, representing over 47,000 artists worldwide. Roughly 804,000 works sold, yet the majority of those sales occurred at modest prices.

Approximately 80% of works sold for under $3,500, and the median price was below $1,000.

These statistics tell a story that often gets lost beneath headlines about record-breaking sales. The art market appears vast, but its economic center is surprisingly narrow.

Lévy describes the system as "a steep, asymmetric architecture where visibility is concentrated and participation is episodic."

Much of the market's transaction volume comes from prints, editions, estates, and repeated consignments—works circulating frequently enough to create the impression of constant activity.

The effect is a kind of optical illusion.

The market appears deep, but in reality the same works and the same artists often circulate repeatedly through auctions and secondary sales. Liquidity, Lévy suggests, is frequently "recycling, not expanding."

The Attention Machine

The art world has become remarkably skilled at measuring visibility.

Attendance numbers. Social media reach. Auction lot counts. Database rankings.

But these metrics tell us more about attention than about transactions.

As Lévy puts it, "crowds are mistaken for demand."

Art Basel Miami Beach 2024

Art fairs provide a perfect example. Galleries may pay six-figure booth fees for the chance to present their artists to thousands of visitors. Sponsorships, hospitality programs, and VIP events create the atmosphere of cultural abundance.

Yet only a tiny fraction of attendees ever buy.

The fair is economically liquid in sponsorships and rented visibility—but not necessarily in art itself.

For galleries and artists, the cost of participating can be substantial (in my experience, the price of a luxury car).

For the fair, the economics are may seem secure regardless of whether sales occur, but poor performance leads to less gallery attendance year over year.

The Real Bottleneck: Conversion

The most compelling idea in Lévy's essay is deceptively simple.

"The art market does not have a demand problem," he writes. "It has a conversion problem."

The gallery director part of my brain winces at that.

Because I know this to be true:

Many people love art. However, far fewer feel comfortable buying it.

Anyone who has attended an art fair or entered a gallery for the first time understands the friction points.

Prices are rarely visible. The etiquette of purchasing is often unspoken. The financial stakes feel high.

Other industries have spent decades removing these barriers.

Luxury fashion built e-commerce platforms with transparent pricing and frictionless checkout. Design marketplaces developed recommendation engines that guide buyers toward objects aligned with their taste and budget.

Cartier 'Baignoire Watch' 2023 Ad Campaign

The art world, by contrast, still relies heavily on informal mentorship: a knowledgeable gallerist, a collector introducing a friend, a curator offering context.

When that guidance exists, new collectors often emerge quickly. When it doesn't, interest remains admiration rather than participation.

Once more, with attention (read: marketing 'eyeballs'), visitors may enter a gallery or fair booth, but their intention is to be present, not to patronize.

We've landed on a strange economy of attention that doesn't pay, a paywall that seems opaque, and a system that still has very little guidance toward outsider navigation.

The Disappearing Middle

Another consequence of the market's architecture is increasing concentration at the very top.

For nearly two decades, the ecosystem has become more dependent on a relatively small group of ultra-wealthy buyers.

Growth has not disappeared—it has simply accumulated at the highest tier.

Lévy writes that "almost all of it accrues to the top 0.1%, while the system beneath is asked to survive on attention alone."

This concentration has ripple effects.

When the number of active collectors is narrow, even minor shifts in sentiment can affect the entire ecosystem—from galleries to artists to fairs.

Meanwhile, many potential collectors quietly migrate elsewhere. Design, furniture, fashion, and collectible objects have built infrastructures that feel easier to navigate.

Even wine and car collections feel more 'novice friendly' when conducting a quick search on the internet.

These markets invested in transparency, recommendation tools, and buyer confidence.

The art world, by comparison, often continues to treat opacity as a feature rather than a barrier.

The Data Trap

Ironically, the digital age has introduced a new kind of risk.

Auction results that once disappeared into archives now remain permanently visible online.

Lévy warns that "a single low-priced sale becomes a public benchmark, indexed indefinitely by search engines, databases, and advisory dashboards."

An early or distressed sale—perhaps the result of a closed gallery or estate liquidation—can quietly define an artist's perceived market level for years.

Context disappears. Circumstance fades. The number remains.

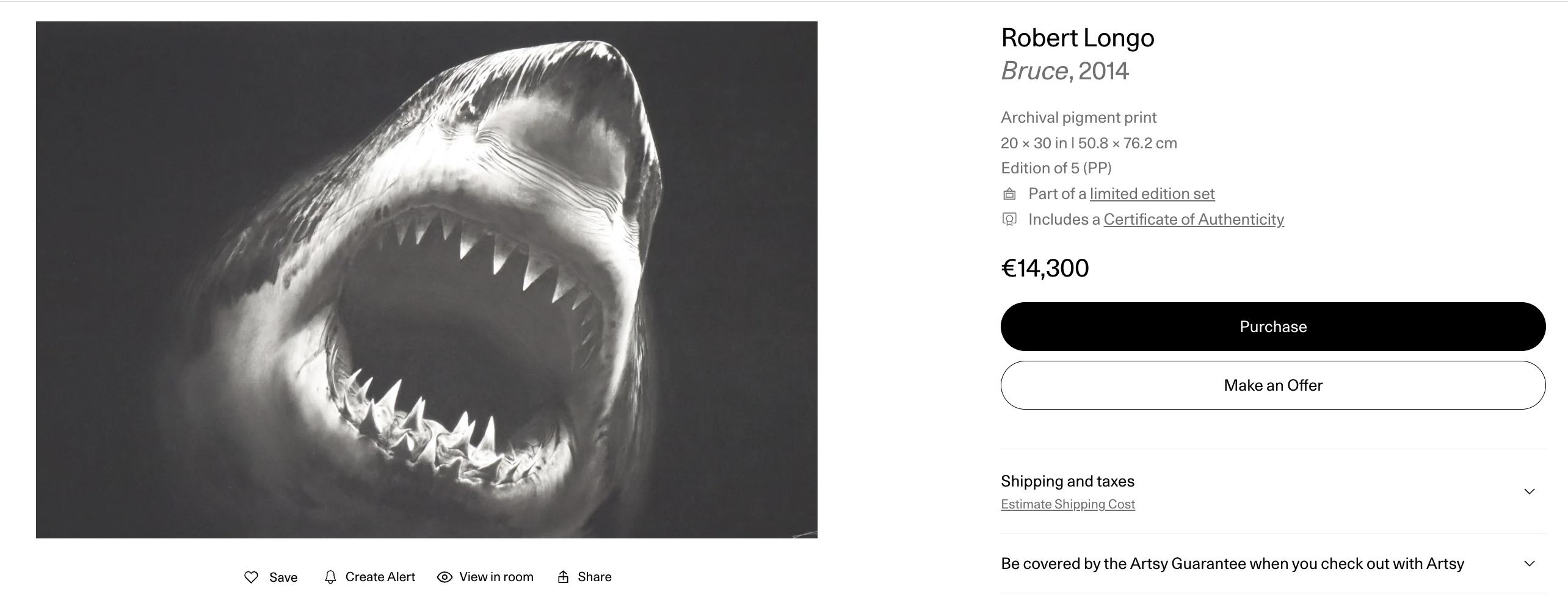

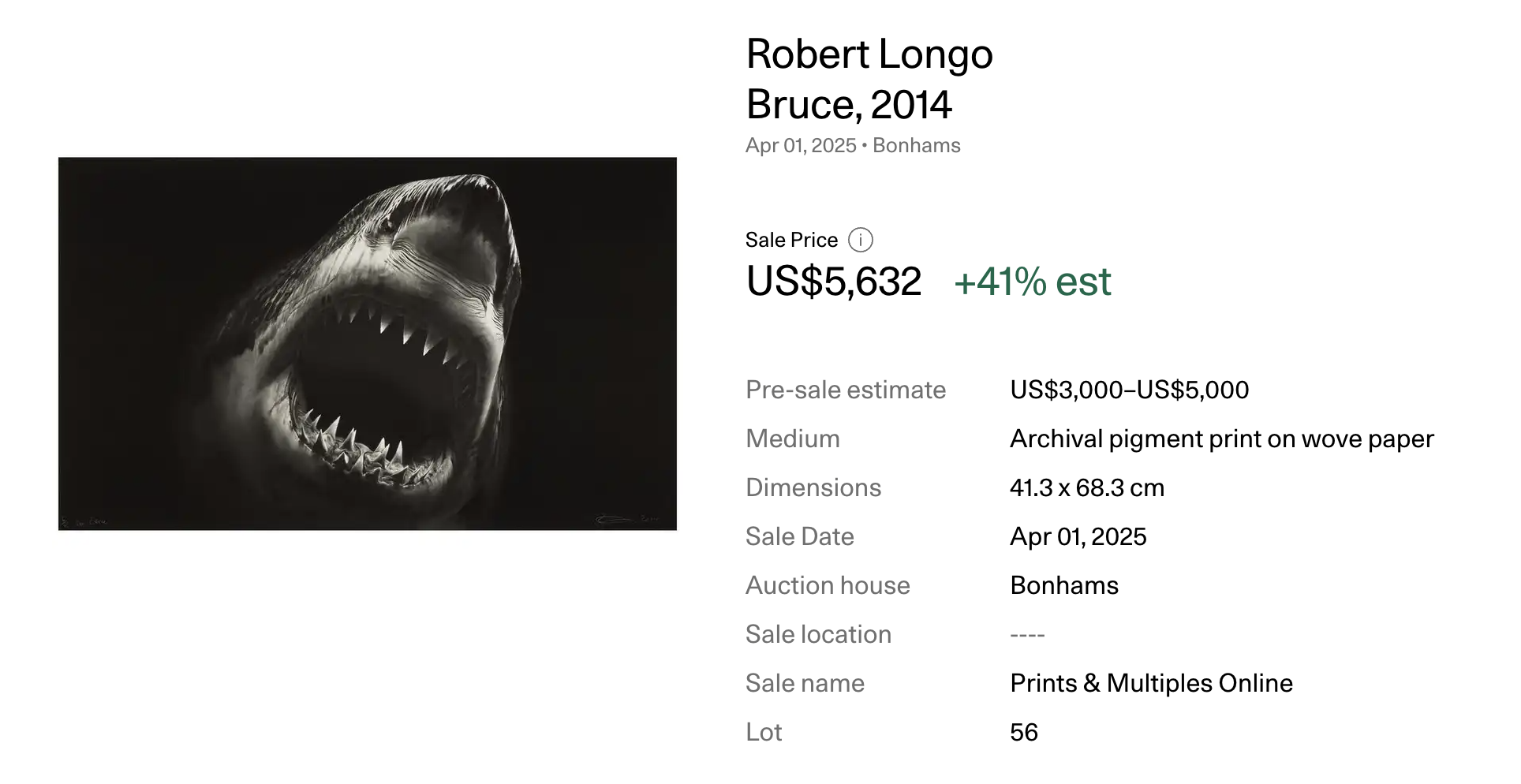

As a gallerist, I can't tell you how many conversations I've had that sound like the following:

"I saw an auction lot for half this price ten years ago…" "What kind of return will I get on this piece in 5 years?" "What is the average price I could get for this at auction?"

A side by side comparison of an auction result + current listing of Robert Longo's "Bruce", 2014.

And listen, these are important questions to ask AND field for those of us in the industry. I really, truly believe in the adage of no dumb questions.

However, if a conversation starts here, we've lost the plot.

Digital transparency, intended to democratize information, can sometimes reinforce inequality by freezing momentary conditions into permanent data points.

Meaning, once an auction result is posted—it permanently becomes a datapoint of value far more understandable than the years spent in self-study, or at a University, the pain of trial and error, or perhaps most measurably, the financial burden of maintaining a regular artistic practice.

The Real Question

Interest in art has never been higher.

Millions attend museums and fairs each year. Millions more follow artists online.

The challenge facing the art world is not (and really, never has been) whether people care.

The challenge is whether the structures of the market will evolve enough to welcome those people as participants rather than spectators.

Because if the art world does not build those systems itself, Lévy warns, they will eventually be built by others—technology platforms, financial intermediaries, and data companies whose incentives may look very different from the slow, relational nature of art.

The future of the art market, in the end, may not be decided by taste.

It may be decided by who builds and adapts the systems—and for whom.